CPI, Recovery in Kharif acreage, Weak FDI, Outward Remittances and more...

CPI, Recovery in Kharif acreage, Weak FDI, Outward Remittances and more...

This Week In Data #31

In this edition of This Week In Data we discuss:

The spike in July CPI and what it means for interest rates

Recovery in Kharif crop acreage

Continued weakness in FDI

Spike in outward remittances in June

More weak data out of China

The July CPI was the key data release for the week. As expected, headline CPI rose sharply to 7.4% YoY up 250bps from the 4.9% YoY level in June. While a sharp uptick in inflation in July was expected, the quantum of the uptick was much higher than consensus expectation. However, the exact CPI print for July is practically irrelevant. It wouldn’t have mattered if the print was 8% or 7%. This is because almost the entire uptick in July was due to the sharp increase in vegetable prices. And this was known.

And as the chart below shows, vegetable prices tend to have these sharp swings. In June, the vegetable price component of CPI was close to its long-term trend line. And in July it is significantly above. And if history is any guide, in 3-4 months, the price level will be back closer to the trend if not lower.

This spike in inflation is thus to be completely ignored. It does not justify a rate hike. What will justify a rate hike is an expectation that this spike in inflation is likely to last beyond 1-2 quarters either by it persisting or by it getting transmitted to other categories. The current hawkish pause stance of monetary policy will thus continue for the foreseeable future.

It has been a few weeks since we last did a check on Kharif sowing and the situation has improved since. As of yesterday, overall Kharif acreage is unchanged from last year. That is an improvement since we last checked with acreage was down 4-5% YoY.

Rice acreage is now up 4% YoY and that of Coarse cereals has increased 2% YoY. Pulses acreage however continues to lag and is currently 9% below last year. From an inflation perspective, this is the major worry. Oilseeds acreage is also down but by a modest 2% YoY. And after two years of strong growth, Sugarcane acreage is up just 1% YoY so far. The kharif sowing season is now drawing to a close and thus these numbers are unlikely to change materially in the next few weeks.

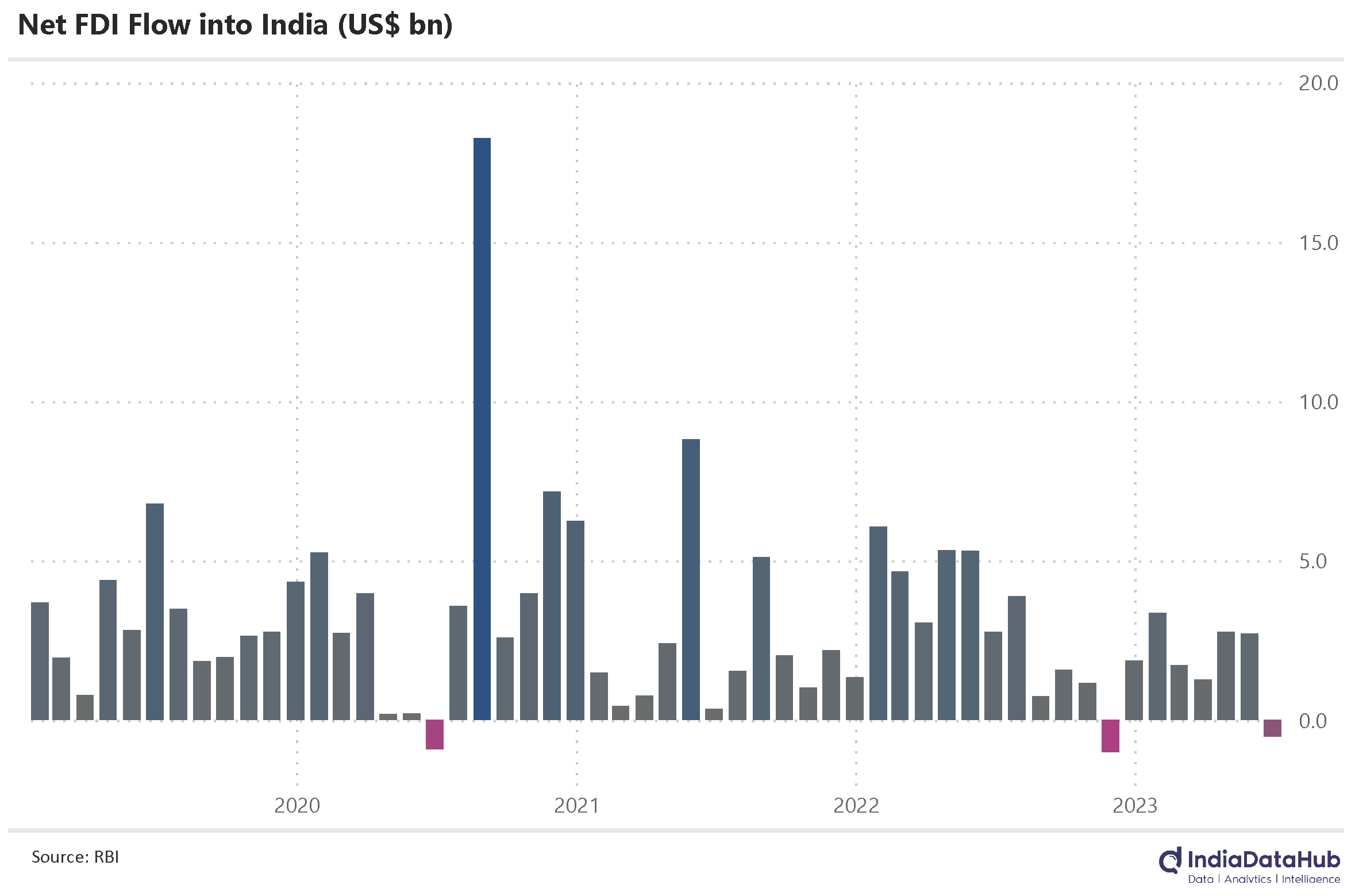

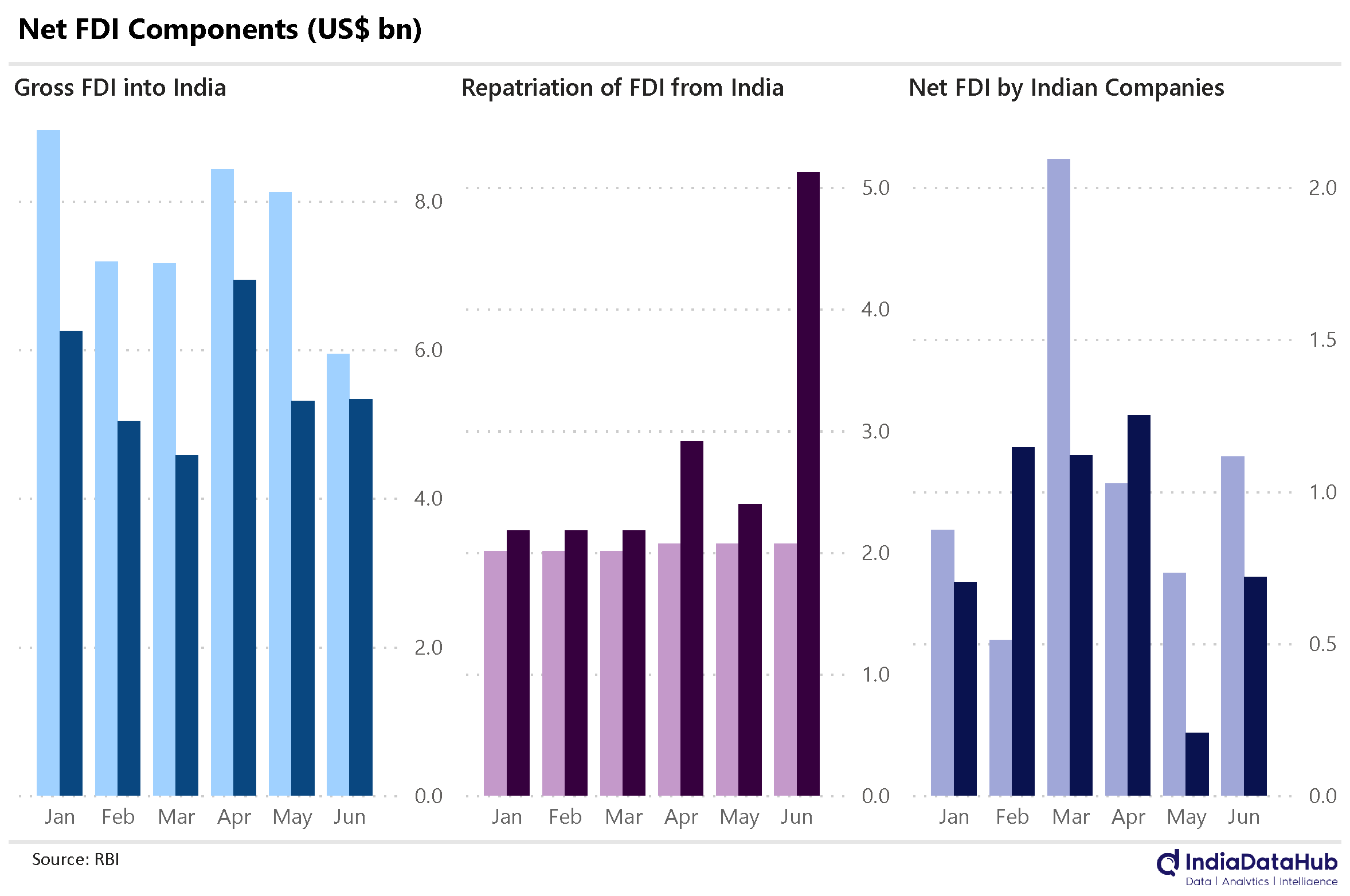

The disappointing trend in FDI continues. June saw negative net FDI in India. This means more money went out of India than came into India. This is only the sixth time in the last 12 years that net FDI has been negative. And two of those occasions were in the past year – June this year and November last year.

The reason for the negative FDI was a big jump in the repatriation of existing FDI out of India. June saw a total of US$5bn of existing FDI investments being repatriated out of India, the highest ever. That said, gross FDI in India continued to decline. June was the sixth consecutive month of decline. Gross FDI into India has declined in 10 of the past 12 months.

The divergence between portfolio investments on the one hand, which continue to remain strong, and FDI on the other hand which continues to decline couldn’t be starker.

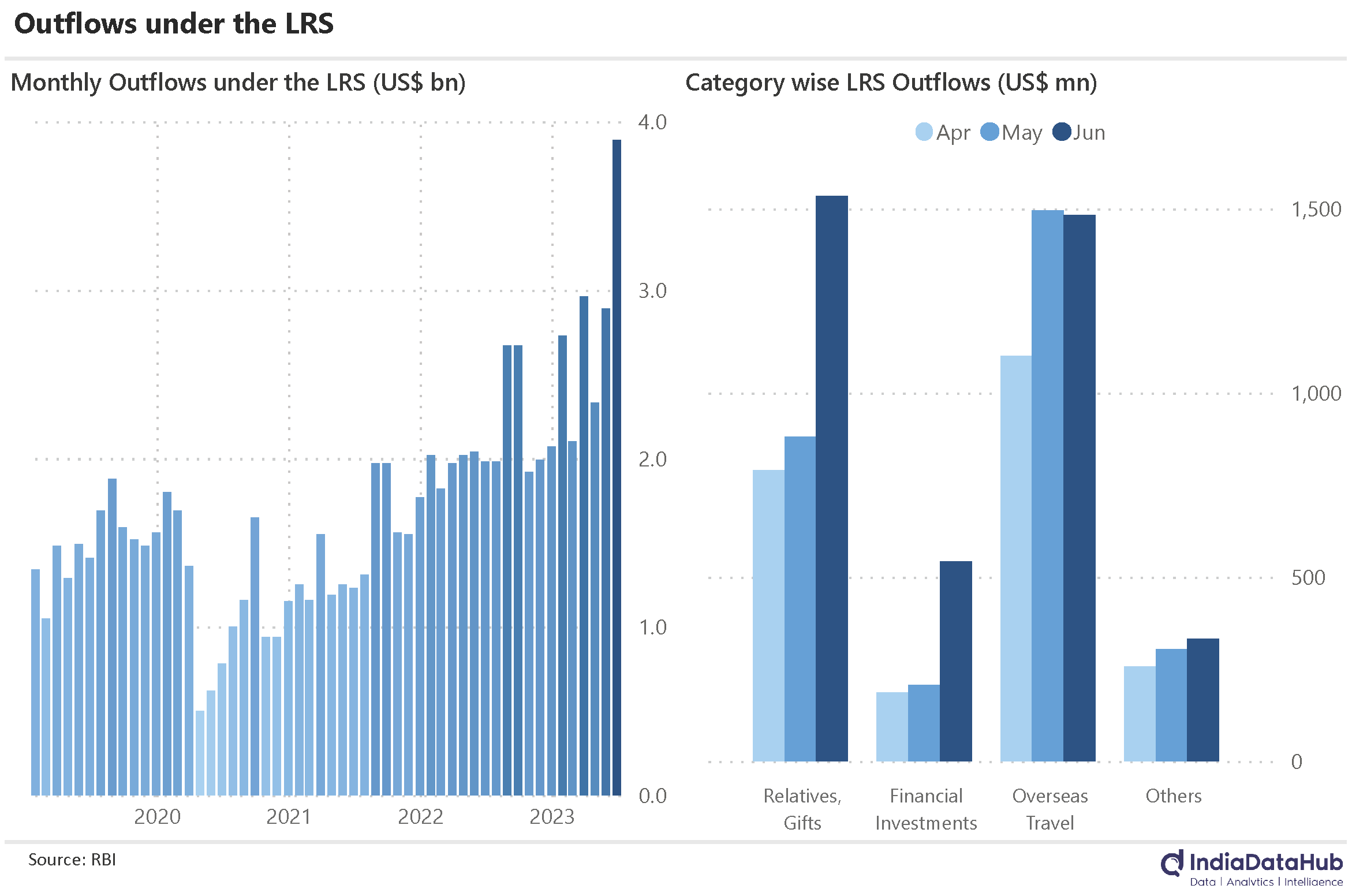

This year’s Union Budget introduced (and in some cases increased) the tax collection at source on remittances under the RBI’s Liberalised Remittance Scheme. This was due to come into effect from 1st July (although at the end of June, the government gave significant relaxation). But anticipating the higher tax deduction from July, June saw a big increase in outflows.

While the average monthly inflows between Mar-May were US$2.7bn, June saw outflows of almost US$3.9bn. That is an additional US$1.2bn remitted outside India in just one month. The entire increase in outflows was from two categories – overseas financial investments and gifts or transfers to relatives as the chart below shows.

Essentially smart money shifted outside India to either avoid the higher tax deduction or the reporting requirements or both. Wealth managers must have worked overtime in June!

This past week was the second consecutive week of weak Chinese data. Industrial production grew 3.7% YoY in July, as against 4.4% in June and the unemployment rate ticked up to a 4-month high of 5.3%. Growth in retail sales and fixed asset investment was also weaker than expected. Not surprisingly then, as we had speculated last week, the PBoC became the first major central bank to ease monetary policy. It cut its short-term policy rate by 10bps and cut the rate on 1-year loans by 15bps.

That’s it for this week. Next week is likely to be a quiet week for data flow. So we will try and dig out something interesting to talk in this newsletter. Have a good weekend…